Behind the Data – COVID’s long impact on Irish household savings

Tiernan Heffernan*

April 2025

This Behind the Data examines recent trends in Irish household bank deposits, and finds that while on average euro area households have now used up much or all of their excess bank deposits accumulated during the COVID-19 period, there is little evidence that this has occurred in Ireland.

A significant accumulation of household deposits has been a feature of the Irish economy for a number of years. This trend was supercharged during the period of the COVID-19 pandemic when Irish deposit accounts swelled, at their height increasing by an annual figure of €15.5 billion or 13.8 per cent. A Central Bank Economic Letter by Simone Saupe and Maria Woods (PDF 637.84KB) found Irish household deposit accumulation to be amongst the highest in the euro area during 2020 and 2021. Since the pandemic, this growth, though still positive, has tempered significantly. We examined how this has played out in Ireland and the euro area, and the current status of ‘excess deposits’ accumulated during COVID-19. This was primarily done using deposits data collected by the Central Bank of Ireland and other National Central Banks (NCBs) in the euro area. Additional data from the CSO and other sources is used to provide further context.

The Data

HH deposit accumulation during COVID, and subsequent trends

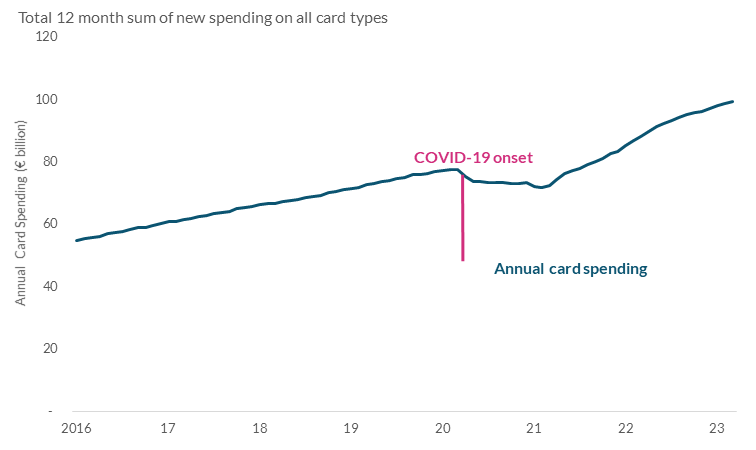

Irish household bank deposits grew at significantly increased rates during COVID-19, relative to prior periods. This scenario occurred in many countries across the world, and is generally agreed to have been driven by two factors. The first is government COVID-19 financial support measures. Cahill and Lydon describe how incomes in Ireland would have fallen during the COVID-19 period (PDF 565.14KB) by significantly more than they actually did without these supports. The second factor is the COVID-19 lockdowns themselves, which reduced the ability of households to spend their income and savings. The effect of the lockdowns can be seen in the below chart which shows that although total household card spending has grown steadily over time, it plateaued and even fell during the initial COVID-19 lockdown period.

Chart 1: Annual card

spending dipped noticeably during COVID-19

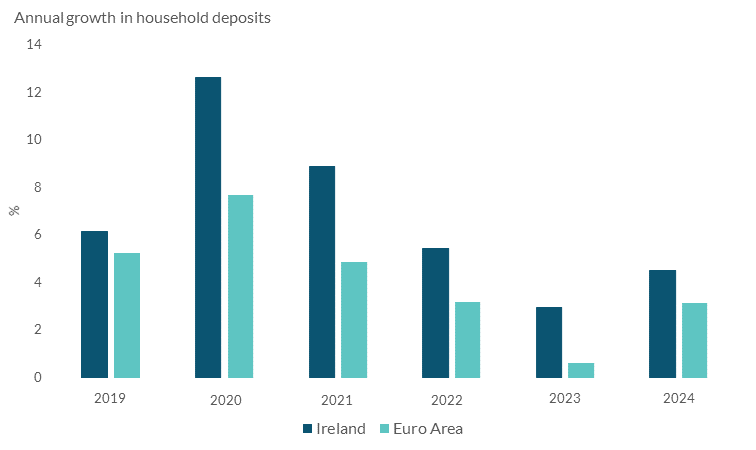

In 2019, the year immediately prior to the COVID-19 pandemic, Irish household bank deposits grew by 6.1 per cent. This reached 12.6 per cent and 8.9 per cent in 2020 and 2021 respectively. The 12-month growth rate peaked at 13.8 percent in the year to February 2021. Countries around the euro area also saw a deposit accumulation during the COVID-19 pandemic, and slowdown of deposit growth, or even a decline in deposits, in subsequent periods. Although the nature of the euro area trend was similar to that of Ireland, the levels of growth across the period were always lower in the euro area than those seen in Ireland.

Chart 2: Irish deposit growth

rates are consistently above the euro area average

These increased growth rates led to the accumulation of what have been variously referred to as ‘excess deposits’, ‘COVID savings’ as well as a variety of other terms. There is no single agreed methodology for calculating this value, though the phenomenon has been noted across many economies. It should be noted that we are focusing specifically on bank deposits in this paper, a large and highly liquid portion of COVID excess savings. COVID impacts may also be seen in other forms of saving too, such as purchase of less liquid assets.

Defining the COVID-19 period as the time between March 2020 and May 2022, we calculated the excess bank deposits figure for Ireland at €13.8 billion1. The annual growth rate of deposits in Ireland during COVID-19 more than doubled over its pre-COVID rate. The increase in the euro area deposit growth rate was still substantial, although much lower than the figure for Ireland. One partial explanation for the higher increase in bank deposits in Ireland relative to the euro area average may be the higher preference of Irish households to keep their savings in more liquid assets as discussed previously in the Central Bank’s Quarterly Bulletin (PDF 548.17KB).

It is important to note here that these are increases in aggregate deposit levels, and that a large number of households would not have seen an increase in their deposit holdings during COVID. More stratified information on household wealth can be seen in the Central Bank’s distributional wealth data.

What has happened to the accumulated deposits since then?

There has been much discussion recently about how these excess deposits have been and are being used since the end of the COVID-19 restrictions, the effect they have had on the economy, and whether and when they will be exhausted. In some countries, it does appear that these excess funds have now reduced or have even been eliminated, as estimated by deposit accumulation rates having fallen below 2018-2019 (pre-COVID) levels for a sufficient period of time. In fact, according to the San Francisco Federal Reserve’s latest estimates, pandemic excess savings remaining in the U.S. economy have now turned negative.

It may have been expected that the utilisation of these excess deposits in Ireland would have been particularly strong, given the high amounts accumulated. The data suggests that this has not been the case. Between June 2022 and December 2024 deposits increased at a monthly average of €514 million. This is actually greater than the pre-COVID accumulation level. This may suggest that either households are not currently spending the savings accumulated during the COVID-19 period, or that in spite of spending these deposits, the trend in deposit accumulation more generally has shifted upwards sufficiently to counterbalance the additional drawdowns.

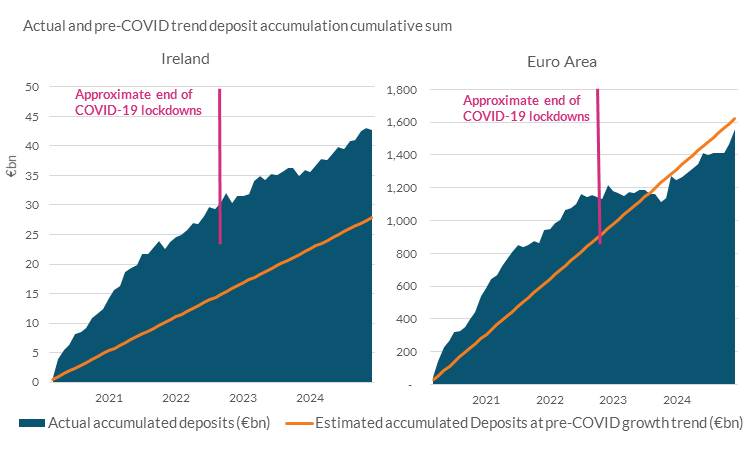

To put this another way, had Irish households continued to accumulate deposits at the volumes which they had done between 2018 and February 2020 (pre-COVID), they would have added €27.9 billion to the stock of household deposits since March 2020 (beginning of COVID period). Instead, they have added €42.7 billion over this COVID and post-COVID period. Euro area households would have accumulated just over €1.6 trillion at pre-COVID trend accumulation levels, but in the end added just under €1.6 trillion. It appears therefore that on average, euro area households have now consumed the entirety of these liquid excess bank savings accumulated during COVID, whereas Irish households still hold €14.8 billion in deposits more than we would have expected based on trends prevailing immediately prior to the COVID-19 period.

Chart 3: Irish households still hold significant excess deposits whereas euro area households have spent theirs

There are a couple of factors which could be helping to support nominal bank deposit accumulation in the post COVID-19 period.

- Firstly, earnings data from the CSO shows that average weekly earnings were €980 in Q4 2024, a 25 per cent increase on pre-COVID average weekly earnings of €786 in Q4 2019. Therefore if households were saving the same proportion of their gross income as they were pre-COVID, we would expect to be seeing higher nominal deposit inflows than in the pre-COVID period.

- Secondly, there has been a significant change in population since the pre-COVID period. CSO data shows that the population in Ireland has increased by almost 7 per cent relative to the pre-COVID period. Household savings accumulation levels have increased by a similar amount between the pre and post-COVID periods.

These factors may help to explain why nominal deposit increases have held up post-COVID. However, neither seem to sufficiently explain the lack of usage of excess COVID bank deposits in Ireland relative to the euro area. Eurostat data suggests the euro area has seen similar wage increases to those seen in Ireland, and the population change levels are insufficient to explain the significantly divergent trends in Ireland relative to the euro area.

The lack of excess deposit wind down seems more reasonably attributed to aggregate behavioural decisions of households. Household saving rates have remained high throughout the post COVID period. Central Bank analysis (PDF 1.05MB) suggests that this may be due to demographic trends among other factors. Addtionally, this same analysis piece also finds that much of the consumption that was withheld during COVID seems to have been foregone entirely, rather than postponed. Spending post-COVID is reaching levels similar to pre-pandemic, rather than significantly exceeding it.

Conclusion

This paper shows that in the case of Ireland, excess bank deposit accumulation was likely significantly higher than it was on average across the euro area, and that utilisation of these excess deposits has been less apparent in the post-COVID period. Population growth and increases in nominal wages may partially explain why households are still accumulating deposits at levels above those seen prior to the pandemic, despite having built up significant excess savings during it. These factors do not seem to fully explain why excess liquid savings drawdown in Ireland has been so muted relative to the rest of the euro area, and there is strong reason to believe that Irish households may still hold significant levels of these excess savings.

*Email [email protected] if you have any comments or questions on this note. Comments from Barra McCarthy, David Duignan, and Jean Cassidy are gratefully acknowledged. Thank you to Brian Kenny and Carlos Luis Navarro Ramirez for checking the calculations used. The views expressed in this note are those of the authors and do not necessarily reflect the views of the Central Bank of Ireland or the ESCB.

[1] This is calculated by taking the average monthly net flow in household deposits during the COVID period, and calculating the difference between this and the average monthly net flow in deposits in the 2 years immediately prior to the COVID lockdowns. These monthly differences are then summed for the duration of the COVID period (approximated as March 2020 - May 2022).

See also: