Behind the Data – Low and slow: Irish household deposit preferences and their response to the changing interest rate environment

Tiernan Heffernan*

April 2025

This Behind the Data examines recent trends in Irish household deposits, and specifically the types of deposit accounts typically held by Irish households, how this compares to the euro area, and the consequences of these differences. There were also a series of increases in ECB reference interest rates beginning in July 2022 which may have impacted these trends.

We found that while the increased interest rates did attract Irish household to place their deposits in longer-term deposit accounts to some extent, they still lag far behind the euro area average in this respect. This trend may also have been impacted by Irish rates often being lower than average euro Area rates historically, though this is not the case in the most recent data. We approximate that Irish households’ preference for shorter-term, more accessible deposit account types relative to average euro area household behaviour cost them almost €800 million in unearned interest in 2024 alone.

The Data

The composition of household deposits

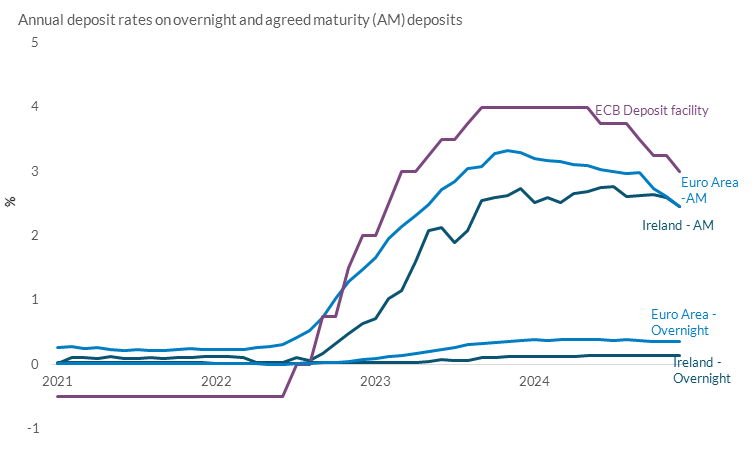

In July 2022 the ECB began what was to become a series of interest rate increases. The deposit facility rate went from -0.5 per cent to a level of 4 per cent in just over a year. These rate increases would gradually impact the rate offered to households by commercial banks on their current account and savings balances. This happened in both Ireland, and the broader euro area, though average euro area savings rates had until recently remained above those offered by Irish banks (Chart 1).

Chart 1: Euro Area deposit rates have generally been higher than Irish rates

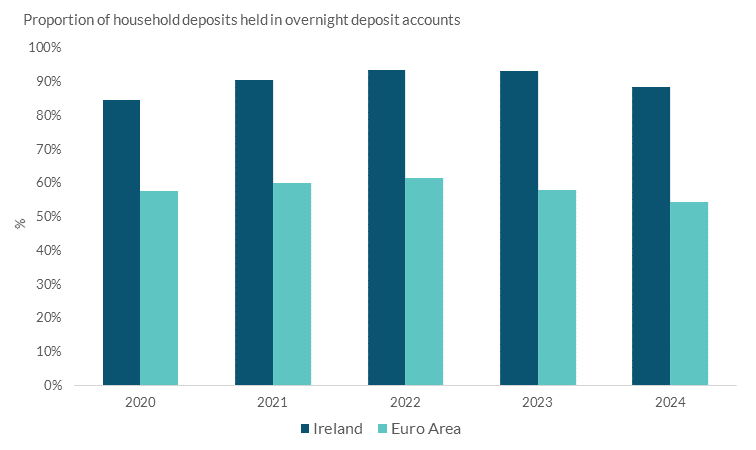

Irish households have long held a very high proportion of their deposits in current accounts or other easy-to-access but low interest account types. As shown in Chart 2, the share of overnight deposits in total has been close to 90 per cent in recent years, making Ireland an outlier in the broader euro area, where overnight deposits have a share of around 55 per cent. Interest rate increases from mid-2022 enticed households to begin to shift their bank savings from overnight into longer-term savings accounts. This transition has happened slowly in Ireland however, and the proportion of deposits being held in overnight accounts (which earn much lower rates of interest) remains very high.

Chart 2:1 Irish households hold more of their deposits in lower interest account types

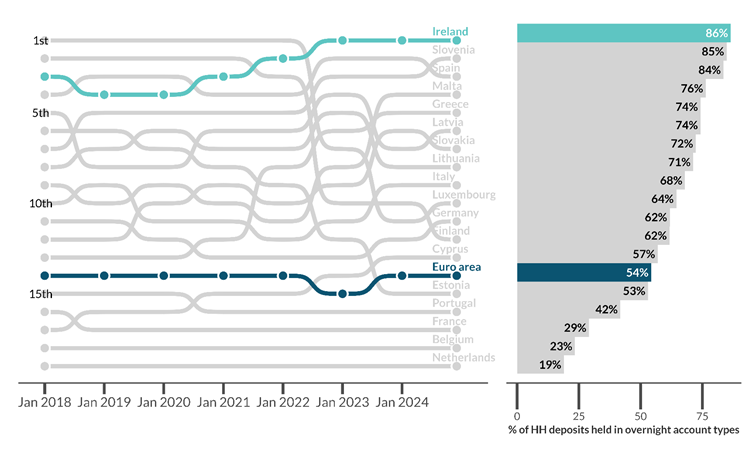

Chart 3: Ireland has the highest proportion of household deposits in the overnight deposit category in the Euro area

This long-term interest rate differential which had previously existed, and can be seen in chart 1 above, may help to explain why Irish households have a higher tendency than average euro area households to keep their deposits in overnight accounts, which have fewer barriers to accessing funds. Irish households are giving up less in terms of unearned interest, as the rates available are lower, in order to gain the increased flexibility that immediate access to their funds offers.

This lower interest rate being offered by banks on deposits, and the likely related reluctance of Irish households to lock their savings into longer term accounts with more restrictions on access, has significant consequences on households in terms of interest earned. The amounts in question are difficult to quantify exactly, however we estimate that Irish households earned approximately €532 million in interest in 2024. This is calculated by taking the average volumes in each different deposit maturity category over the year, and applying the corresponding average interest rate for each deposit maturity category to these volumes2. If we were to do the same exercise, but assume Irish households held their deposits across the various maturity categories in the same proportions as the average euro area country’s households, this interest earned in 2024 would be significantly higher. This is due to euro area households’ preference for longer term higher interest account types relative to Irish households. In this situation Irish households would have earned €1,320 million in bank deposit interest in 2024, or €788 million more than the actual estimate.

Additionally, as the average euro area interest rate on deposits was higher than the average Irish rate for 2024, we can estimate that even with their current maturity preferences, they would have earned an additional interest amount of €444 million in 2024, had they been remunerated at the average euro area bank interest rates.

Another possible consequence of Irish banks’ previous lower deposit rates is the increasing trend for Irish households to place deposits at digital banks or neobanks3, which may offer higher interest rates. Levels of Irish deposits held at these banks remain very small in comparison with deposits held domestically (still just approximately 3 per cent of total deposits), though we are seeing rapid rates of growth in Irish households deposits in such banks4.

Chart 4: Irish households are increasing their deposit holdings in non-Irish banks (proxy for neobanks)

Conclusion

Higher bank deposit rates, resulting from the ECB’s interest rate increases from mid-2022, have slowly begun to influence Irish households into moving some of their overnight deposits into longer-term savings accounts. They still lag significantly behind their euro area peers, however, in terms of the proportion of deposits held in these longer-term accounts and this has resulted in Irish households missing out on potential improved returns. Indeed Irish households now have the highest proportion of their bank deposits in overnight accounts out of any country in the euro area. Before the ECB interest rate hikes from mid-2022, a decade of very low interest rates meant that the difference between overnight and term deposit rates was minimal, so households had little incentive to hold longer-term deposits. Irish households have been slower than their euro area counterparts to respond to rising term deposit rates since 2022, although until recently the average interest rate on term deposits in Ireland remained lower than the euro area average. These interest rate differentials also may have nudged Irish households towards holding their deposits at neobanks which often offer higher rates on deposits and additional online services.

*Email [email protected] if you have any comments or questions on this note. Comments from Barra McCarthy, David Duignan, and Jean Cassidy are gratefully acknowledged. Thank you to Brian Kenny and Carlos Luis Navarro Ramirez for checking the calculations used. The views expressed in this note are those of the authors and do not necessarily reflect the views of the Central Bank of Ireland or the ESCB.

[1] Ireland figures based on deposits by domestic households and euro area figures based on deposits by euro area households.

[2]The underlying data are collected by the Central Bank to meet our statistical reporting obligations to the ECB. The data on volumes are covered by the ECB BSI Regulation, and the data on interest rates are covered by the ECB MIR Regulation.

[3] Here we are referring to institutions which have banking licences, but predominantly operate online.

[4] We use deposits held in other euro area banks to approximate the trends in deposits held at neobanks. It does not include deposits at domestic resident neobanks, so will therefore underestimate the total value of deposits held at neobanks.

See also:

- COVID’s long impact on Irish household savings